Does Insurance Cover Stolen Cars Your Guide to Coverage

Does insurance cover stolen cars? It’s a question many car owners ask, and the answer is not always straightforward. While comprehensive car insurance is designed to protect you against theft, there are several factors that can influence the amount of compensation you receive. Understanding the intricacies of comprehensive coverage, including its limitations and exclusions, is crucial for making informed decisions about your car insurance.

This guide delves into the world of car insurance and stolen vehicles, exploring the different aspects of coverage, the factors that impact compensation, and the process of filing a claim. We’ll also examine alternative options for protecting yourself against financial losses due to theft, providing you with a comprehensive understanding of your rights and responsibilities as a policyholder.

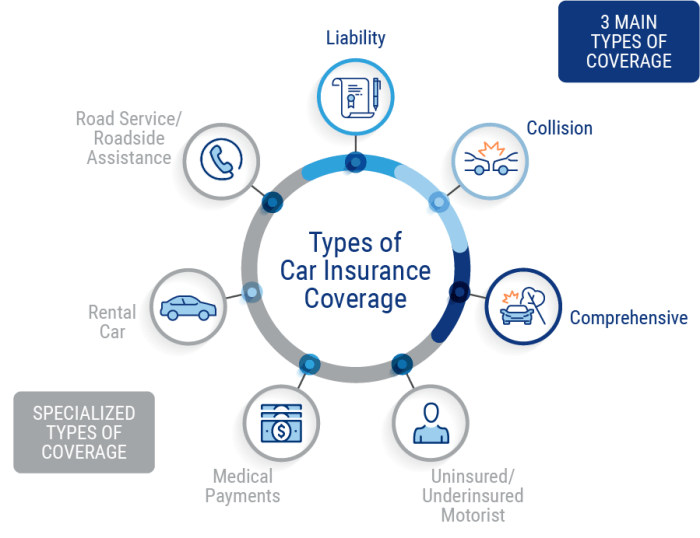

Understanding Car Insurance Coverage

Car insurance is designed to protect you financially in case of an accident, theft, or other incidents involving your vehicle. Different types of coverage offer varying levels of protection, and understanding these options is crucial for choosing the right policy for your needs.

Comprehensive Coverage

Comprehensive coverage is a vital component of car insurance that protects you against losses not caused by collisions. It typically covers damage or loss to your vehicle resulting from events such as:

- Theft

- Vandalism

- Fire

- Hailstorms

- Flooding

- Natural disasters

- Falling objects

- Animal collisions

Exclusions and Limitations

While comprehensive coverage provides extensive protection, it does have limitations. Here are some common exclusions and limitations:

- Wear and tear: Comprehensive coverage generally doesn’t cover damage caused by normal wear and tear, such as a flat tire or a broken windshield wiper.

- Mechanical breakdowns: Comprehensive coverage doesn’t cover mechanical failures, such as a broken engine or transmission.

- Neglect: If your vehicle is damaged due to neglect, such as leaving it unlocked or failing to maintain it properly, your claim may be denied.

- Deductible: You’ll have to pay a deductible, which is a fixed amount, before your insurance company covers the rest of the repair or replacement costs.

- Coverage limits: Comprehensive coverage has limits on the amount your insurer will pay for repairs or replacement. The actual amount depends on your policy and the value of your vehicle.

- Exclusions based on the cause of loss: Some policies may exclude coverage for certain events, such as acts of war or nuclear incidents.

How Comprehensive Coverage Handles Stolen Vehicles, Does insurance cover stolen car

If your vehicle is stolen, comprehensive coverage will typically cover the following:

- Actual Cash Value (ACV): This is the market value of your vehicle at the time of the theft, minus depreciation. You’ll receive payment based on the ACV, not the original purchase price.

- Replacement cost: Some policies offer replacement cost coverage, which means you’ll receive the full cost of replacing your stolen vehicle with a similar model, regardless of its age or condition.

- Rental car reimbursement: Your insurance company may provide coverage for a rental car while your stolen vehicle is being replaced.

Factors Affecting Coverage for Stolen Cars

While car insurance generally covers theft, the amount of compensation you receive can vary significantly. Several factors influence how much you’ll get for your stolen vehicle. Understanding these factors is crucial for making informed decisions about your insurance policy.

Vehicle Age, Make, and Model

The age, make, and model of your car play a significant role in determining the coverage amount. Newer vehicles generally have higher replacement costs, meaning you’ll receive more compensation if they’re stolen. Conversely, older vehicles depreciate in value over time, resulting in lower coverage amounts. Similarly, luxury or high-performance cars typically have higher insurance premiums and coverage limits compared to standard models.

Policyholder’s Driving History and Claims History

Your driving history and claims history can influence the amount of coverage you receive for a stolen vehicle. Drivers with a clean driving record and no prior claims are usually considered lower risk by insurance companies. They may receive higher coverage amounts and lower premiums compared to drivers with a history of accidents or violations. However, it’s important to note that claims history doesn’t always negatively impact coverage. For example, a claim for a minor fender bender might not significantly affect your coverage for a stolen vehicle.

Filing a Claim for a Stolen Vehicle

Once you’ve reported your stolen vehicle to the authorities, you need to contact your insurance company to file a claim. This process helps you initiate the necessary steps to recover your financial losses and potentially replace your vehicle.

Steps to Filing a Stolen Vehicle Claim

You need to act promptly and provide accurate information to ensure a smooth claim process. Here’s a step-by-step guide:

- Contact your insurance company: Immediately contact your insurance company’s claims department. Provide them with the necessary information, such as your policy number, the date and time of the theft, and the location where the vehicle was stolen.

- File a police report: Obtain a copy of the police report filed for the stolen vehicle. This report serves as crucial documentation for your insurance claim.

- Provide documentation: Gather and provide the insurance company with the following documentation:

- Vehicle registration

- Vehicle title

- Proof of insurance

- Any additional relevant documents, such as a loan agreement or lease contract

- Complete the claim form: Your insurance company will provide you with a claim form to complete. Be sure to provide accurate and detailed information about the theft.

- Cooperate with the investigation: Your insurance company may conduct an investigation to verify the details of the theft. Be prepared to provide any additional information or documentation they require.

Documentation Required for a Stolen Vehicle Claim

Providing the necessary documentation is essential for a successful claim. Here’s a list of common documents:

Also Read: Car Insurance Iowa Navigating Your Options

- Police report: This report details the incident, including the date, time, and location of the theft. It also provides evidence of the theft.

- Vehicle registration: This document verifies the vehicle’s ownership and provides information about its make, model, and year.

- Vehicle title: This document proves your legal ownership of the vehicle.

- Proof of insurance: This document confirms that you had active insurance coverage at the time of the theft.

- Loan agreement or lease contract: If you have a loan or lease on the vehicle, you’ll need to provide this document to the insurance company.

- Inventory of belongings: If any personal belongings were stolen from the vehicle, create an inventory list detailing each item, including its value.

- Photos or videos: If you have any photos or videos of the vehicle before the theft, provide them to the insurance company.

Investigation Process and Potential Delays

Once you file a claim, your insurance company will initiate an investigation to verify the details of the theft. This process may involve:

- Reviewing the police report: The insurance company will review the police report to confirm the details of the theft.

- Contacting witnesses: If there are any witnesses to the theft, the insurance company may contact them to gather information.

- Checking for fraudulent activity: The insurance company may investigate whether the theft was staged or fraudulent.

- Locating the vehicle: If the vehicle is recovered, the insurance company will need to inspect it to assess the damage.

The investigation process can take time, depending on the complexity of the case. Delays may occur due to factors such as:

- Lack of information: If the police report or other documentation is incomplete, it may delay the investigation.

- Multiple claims: If there are multiple claims related to the theft, it may take longer to process each claim.

- Complex investigations: If the investigation involves a complex scenario, it may take longer to gather all the necessary information.

Recovering a Stolen Vehicle: Does Insurance Cover Stolen Car

Insurance companies play an active role in recovering stolen vehicles, working closely with law enforcement agencies to increase the chances of getting your car back.

Procedures for Recovered Vehicles

The process of handling a recovered vehicle depends heavily on the extent of damage it has sustained.

- Vehicles with Minimal Damage: In cases where the stolen vehicle is recovered with minimal damage, the insurance company will typically arrange for its return to you. The company might conduct a thorough inspection to ensure that no further damage has occurred and that the vehicle is safe to drive.

- Vehicles with Significant Damage: If the stolen vehicle has sustained significant damage, the insurance company will likely initiate a claim process. The extent of the damage will determine the course of action. In some cases, the vehicle might be deemed a total loss, and you will receive a settlement based on the vehicle’s value before it was stolen. However, if the damage is repairable, the insurance company will typically cover the cost of repairs.

Determining Vehicle Value and Replacement Cost

The value of a stolen vehicle and its replacement cost are crucial factors in determining the insurance settlement. Insurance companies use various methods to assess the value of a vehicle, including:

- Market Value: This method considers the vehicle’s current market price based on factors like its make, model, year, mileage, condition, and location.

- Actual Cash Value (ACV): ACV is the vehicle’s fair market value minus depreciation. It accounts for the vehicle’s age, mileage, and condition, reflecting its worth at the time of the theft.

- Replacement Cost: This method aims to provide you with the amount needed to replace your stolen vehicle with a similar one. It considers the cost of a comparable vehicle in the current market, including taxes and fees.

Insurance companies often use valuation tools and databases to determine the fair market value of a stolen vehicle. They may also consider expert opinions from appraisers or independent valuation services.

Alternatives to Comprehensive Coverage

Comprehensive coverage is a valuable component of car insurance, but it might not be the most cost-effective option for everyone. If you’re looking for ways to protect yourself against financial losses due to theft without the high premiums associated with comprehensive coverage, consider exploring these alternatives.

Gap Insurance

Gap insurance is a specialized type of coverage that bridges the gap between the actual cash value (ACV) of your car and the outstanding loan balance if your vehicle is stolen or totaled. It’s particularly beneficial for newer vehicles, as their value depreciates quickly, and you could end up owing more than the insurance payout.

- Pros:

- Provides financial protection if your car is stolen or totaled and you owe more than the insurance payout.

- Offers peace of mind knowing you won’t be stuck with a significant debt after a theft.

- Can be purchased separately or bundled with your auto loan.

- Cons:

- Additional cost on top of your regular car insurance premiums.

- May not be necessary for older vehicles with lower loan balances.

- Coverage may have limitations, such as a maximum payout amount or a specific time frame.

Deductible Waiver

A deductible waiver is a feature that eliminates or reduces your out-of-pocket expenses in the event of a claim. This can be a valuable option if you’re concerned about the potential cost of a deductible after a theft.

- Pros:

- Reduces or eliminates your out-of-pocket expenses after a claim.

- Provides greater financial protection in case of a theft.

- Can be added to your existing car insurance policy.

- Cons:

- Increases your insurance premiums.

- May not be available for all types of claims.

- Coverage may have specific limitations, such as a maximum payout amount or a specific time frame.

Increased Liability Coverage

Liability coverage is a standard component of most car insurance policies. Increasing your liability coverage can help protect you financially if you’re involved in an accident that results in significant damage to another vehicle or injuries to another person.

- Pros:

- Provides greater financial protection in case of an accident.

- Can help reduce the risk of financial hardship if you’re found liable for damages.

- May be required by law in some states.

- Cons:

- Increases your insurance premiums.

- May not be necessary if you have a low risk of accidents.

Table Comparing Coverage Options

| Coverage Option | Key Features | Benefits | Limitations |

|---|---|---|---|

| Comprehensive Coverage | Covers theft, vandalism, and other non-collision damages. | Provides comprehensive protection against a wide range of risks. | Higher premiums. |

| Gap Insurance | Covers the difference between the ACV and the loan balance. | Protects against debt after a theft or total loss. | Additional cost, may not be necessary for older vehicles. |

| Deductible Waiver | Eliminates or reduces out-of-pocket expenses after a claim. | Provides greater financial protection. | Increases premiums, may not be available for all claims. |

| Increased Liability Coverage | Protects against financial losses due to accidents. | Provides greater financial protection. | Increases premiums, may not be necessary for low-risk drivers. |

Being a victim of car theft can be a stressful and overwhelming experience. However, understanding your car insurance coverage and knowing your rights can help you navigate this challenging situation. By carefully reviewing your policy, understanding the factors that affect compensation, and following the proper procedures for filing a claim, you can increase your chances of receiving the necessary financial assistance to recover from the loss of your stolen vehicle.

Top FAQs

What happens if my stolen car is recovered?

The process for handling recovered vehicles depends on the extent of the damage. If the car is recovered undamaged, you’ll likely receive your vehicle back. However, if it’s damaged, the insurance company will assess the damage and determine if it’s worth repairing or if it should be declared a total loss.

What if my car is stolen and I have a loan on it?

If you have a loan on your car, the insurance company will typically pay the lender the remaining balance of the loan, and you will receive any remaining compensation after the loan is paid off. This is important to understand, as you may not receive the full value of your car if you still owe money on it.

Can I get a replacement car if my stolen car is declared a total loss?

Yes, if your stolen car is declared a total loss, your insurance company will provide you with the actual cash value of your vehicle, which is based on its market value at the time of the theft. You can then use this money to purchase a replacement vehicle.