Connecticut Car Insurance

Connecticut Car Insurance: Navigating Policies, Coverage, and Costs

Welcome to the world of Connecticut car insurance—a realm where understanding policies, coverage options, legal requirements, and cost-saving strategies intersect to ensure your experiences on the road are accompanied by peace of mind. Whether you’re a new driver embarking on your first vehicle journey or a seasoned motorist reevaluating your insurance needs, this guide aims to provide clarity in the often cloudy skies of auto insurance.

In the heart of New England, Connecticut presents a unique landscape for car insurance enthusiasts and consumers alike. With its distinct seasons affecting driving conditions, a woven tapestry of urban and rural roads, and specific state mandates, Connecticut’s insurance landscape is like no other. As such, diving deep into the intricacies of car insurance here isn’t just beneficial—it’s vital. Within this blog post, we’ll embark on an informative journey, peeling back the layers of confusion that often shroud the topic of car insurance.

Also Read: Good Math America

Our exploration will begin with an overview of Connecticut’s mandatory insurance requirements. The state law dictates certain minimum levels of liability insurance that every driver must carry, and understanding these can save you from legal headaches and financial losses. But minimum coverage may not be sufficient to fully shield you from potential damages or lawsuits, so we’ll also delve into the nuances of additional insurance options that could enhance your coverage and provide broader protection.

With the required coverage as our foundation, we will then shift our focus to the myriad of insurance providers in Connecticut. Each company offers its own suite of policies, discounts, and customer service experiences. So how do you choose the right one? We’ll discuss criteria for evaluating insurance companies, from customer satisfaction scores to financial stability ratings, ensuring you find a provider that complements your unique needs and budget constraints.

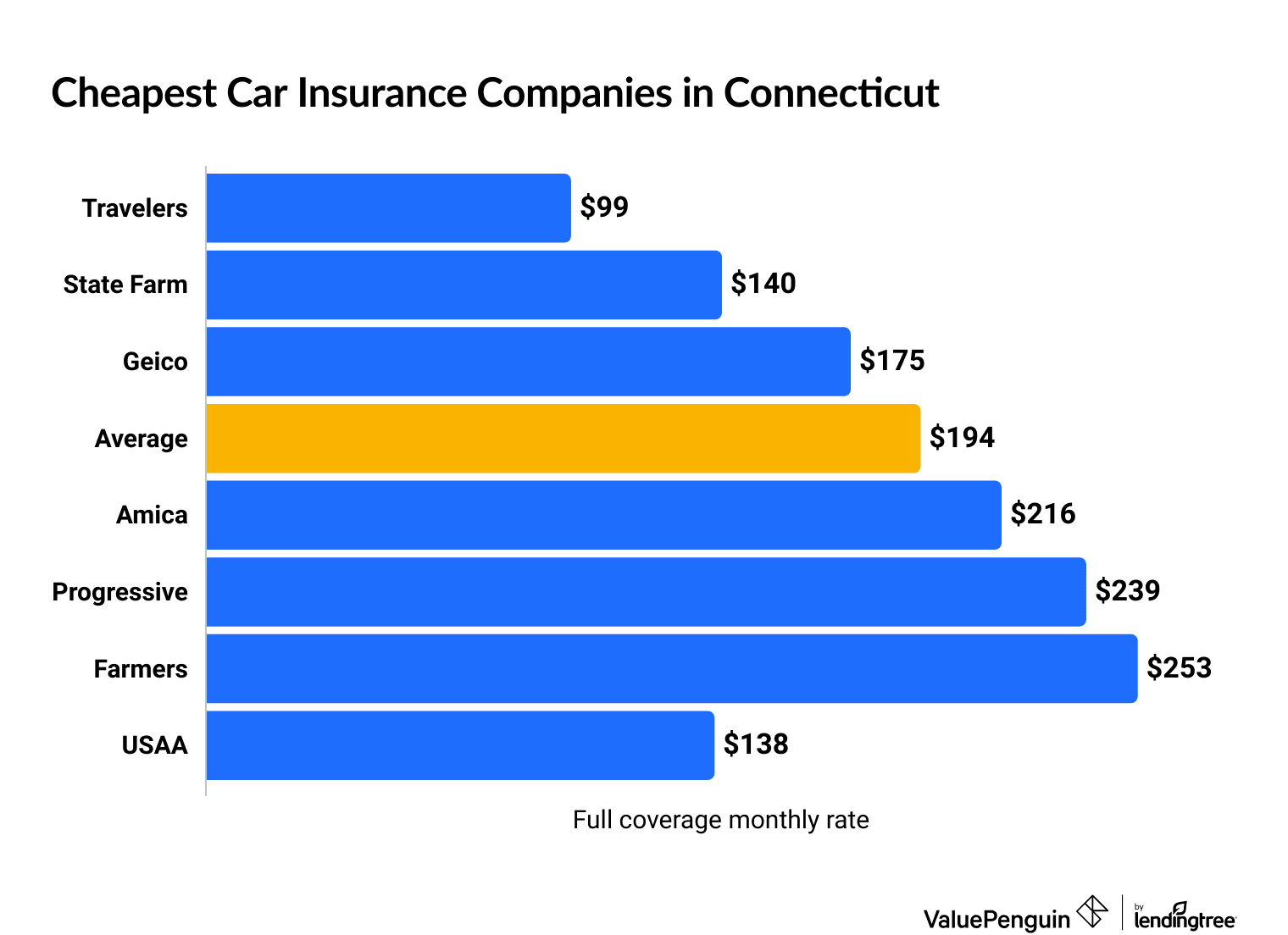

Speaking of budgets, an essential component of this guide will be dedicated to the cost of car insurance in Connecticut. Many factors influence your premium, from personal demographics like age and driving history to geographic factors such as where you live within the state. We’ll offer insights into these elements and share tips on how to lower your premiums without compromising on quality coverage.

Also Read: Good Math Us

Of course, the choices we make today are often influenced by the lessons of the past. Thus, we’ll explore some historical trends in Connecticut’s car insurance industry. Understanding these developments provides context for current market practices and can assist you in anticipating future changes that may affect your policy.

Lastly, no discussion of car insurance in Connecticut would be complete without addressing the technology and innovation reshaping this industry. From telematics and usage-based insurance models to mobile apps and self-service platforms, technological advancements offer new avenues to tailor policies and potentially reduce costs. We’ll examine these innovations and discuss how they are transforming the insurance experience for drivers across the state.

Connecticut car insurance isn’t just a policy—it’s a dynamic ecosystem of regulations, competition, consumer advocacy, and technological change. In the rest of this blog post, we’ll delve deeper into each of these facets to empower you with the knowledge and confidence to make informed decisions. Whether you’re comparing quotes, navigating claims, or simply seeking to understand your policy better, this guide is your compass in the ever-evolving world of car insurance in the Constitution State.

Ready to embark on this insightful journey? Let’s explore the critical elements that comprise a comprehensive Connecticut car insurance strategy.

Also Read: Cindynal Hexapetide Cream

Understanding Connecticut Car Insurance Coverage Requirements

Car insurance is a fundamental requirement for drivers in Connecticut, designed to protect motorists in the event of an accident. Like many states, Connecticut mandates certain types of coverage to ensure that individuals involved in a car accident have financial support for injuries or damages. This section will break down the mandatory requirements you need to know to stay compliant with state laws.

Minimum Liability Coverage

Connecticut requires all drivers to have a minimum amount of liability insurance. This coverage helps pay for other people’s expenses if you cause an accident. The state’s minimum liability coverage limits are:

Also Read: .env

- Bodily Injury Liability: $25,000 per person and $50,000 per accident.

- Property Damage Liability: $25,000 per accident.

Uninsured and Underinsured Motorist Coverage

Connecticut also mandates that drivers carry uninsured and underinsured motorist coverage. This protects you if you are involved in an accident with a driver who either does not have enough insurance or no insurance at all. The required coverage limits mirror those of bodily injury liability:

- Uninsured/Underinsured Motorist Bodily Injury: $25,000 per person and $50,000 per accident.

Medical Payments Coverage

Though not required by state law, medical payments coverage is an option that Connecticut drivers can choose to add to their insurance policies. It covers medical expenses for you and your passengers, regardless of who is at fault in the accident. Many drivers find this coverage beneficial as it provides immediate support following a collision.

Additional Coverage Options

While the state-required coverage forms the foundation, many Connecticut drivers opt for additional protection to safeguard themselves from the numerous risks that come with driving. These optional coverages can increase your financial security and peace of mind.

Collision and Comprehensive Coverage

These types of coverages can be particularly beneficial:

- Collision Coverage: Helps pay for repairs or replacement of your vehicle if it’s damaged in a collision with another vehicle or object.

- Comprehensive Coverage: Covers damages to your car caused by events that are not collisions, such as theft, vandalism, natural disasters, and wildlife.

Many lenders require borrowers to carry these coverages if the vehicle is financed or leased.

GAP Insurance

Guaranteed Asset Protection (GAP) Insurance: Is an option for those who owe more on their car than it’s currently worth. In the event of a total loss, GAP insurance covers the difference between the car’s actual cash value and what you still owe on the loan or lease.

Roadside Assistance and Rental Reimbursement

Beyond the basics, many insurers offer specific perks such as:

- Roadside Assistance: Offers services like towing, tire changes, and battery jumps if your car breaks down.

- Rental Reimbursement: Compensates you for renting a vehicle while your car is repaired after an accident.

Innovations in Connecticut Car Insurance

As the insurance industry evolves, Connecticut drivers are starting to see the integration of technology and new practices into car insurance offerings. These innovations aim to enhance personalization and improve customer experience.

Usage-Based Insurance

One of the most significant changes is the rise of Usage-Based Insurance (UBI) programs. These programs utilize telematics devices or mobile apps to track driving behavior and mileage, allowing insurers to tailor premiums more closely to individual driving habits. More responsible driving often results in lower premiums, providing an incentive for safe driving.

Digital Tools and Services

Many Connecticut insurers are offering mobile apps and online portals for customer’s convenience. These tools make policy management, claims filing, and communication more accessible. Instant quotes, chat support, and digital ID cards are just a few examples of the innovations that are improving service efficiency and customer satisfaction.

Green Discounts and Initiatives

As environmental awareness grows, several insurers provide discounts for eco-friendly practices, such as driving a vehicle with low emissions. Green discounts can apply to hybrid or electric car owners or those who participate in policyholder programs committed to reducing their carbon footprint.

Considerations When Selecting Your Insurance

Choosing the right car insurance in Connecticut depends on a variety of factors. It’s crucial to consider personal needs and financial situation while also understanding the implications of each type of coverage and option. Here are some tips to consider:

- Evaluate your risk factors and driving habits to decide on optional coverages.

- Compare quotes from multiple providers to ensure you’re getting the best rate.

- Read customer reviews and understand the insurer’s reputation on claims handling and service quality.

- Consider taking a defensive driving course which could qualify you for additional discounts.

Taking the time to review these elements can help you make more informed decisions while navigating the Connecticut car insurance landscape.

Connecticut Car Insurance

As we wrap up our comprehensive journey through Connecticut Car Insurance, it’s clear that ensuring you have the right coverage is not just a legal requirement but also a smart financial decision. We began this guide by discussing the unique characteristics of Connecticut’s insurance landscape, governed by both state laws and the competitive nature of insurance providers. By understanding these nuances, drivers can better navigate their options, ensuring peace of mind on the road.

Throughout the main content, we delved deeply into several key aspects of car insurance. We explored the minimum insurance requirements set by Connecticut law, detailing the mandatory liability coverage of 25/50/25 (representing $25,000 for bodily injury per person, $50,000 for bodily injury per accident, and $25,000 for property damage per accident). Additionally, we discussed how these requirements are designed to protect not only you but also other road users, serving as a baseline for financial responsibility.

Beyond the minimums, we highlighted the importance of considering additional coverage options like comprehensive and collision coverage, uninsured/underinsured motorist protection, and personal injury protection. These coverages offer expanded protection, cushioning you from a wider range of unforeseen circumstances, from accidents caused by uninsured drivers to damages resulting from natural disasters or theft.

The guide also tackled the various factors that influence car insurance premiums in Connecticut. We examined how elements like age, driving history, type and age of the vehicle, credit score, and even location can significantly affect your insurance costs. Understanding these factors helps you make informed decisions and possibly take strategic steps to lower your premiums, such as seeking discounts for safe driving or bundling policies with the same insurer.

In addition, we offered practical tips for shopping around for the best insurance policy. We emphasized the importance of comparing quotes from multiple insurers, reading through policy details carefully, and consulting with insurance agents when necessary. Shopping wisely not only ensures you get the best possible rates but also aligns your coverage with your specific needs and financial considerations.

We ended our exploration with a discussion on how technology is shaping the future of car insurance in Connecticut. From telematics and usage-based insurance models to AI-powered customer service platforms, technological advancements are providing more personalized and efficient experiences for policyholders. Keeping abreast of these trends allows you to leverage new opportunities for savings and improved service.

As you reflect on the diverse topics we’ve covered, it’s clear that understanding and managing car insurance in Connecticut requires both attention to detail and an openness to navigating change. The state’s requirements, combined with the evolving landscape of insurance, present both challenges and opportunities. Being informed and proactive in your approach to car insurance ensures not only compliance with legal mandates but also protection for your assets and well-being.

Now, what comes next? A Call to Action!

We encourage you to take the following steps as you continue your journey with Connecticut car insurance:

Review Your Current Policy: Take a close look at your existing insurance policy. Are you adequately covered? Look for gaps that could leave you vulnerable and consider contacting your insurer to discuss modifications.

Explore Your Options: Don’t settle for the first quote you receive. Use comparison tools, reach out to multiple insurers, and gather several quotes to ensure you’re getting the best deal.

Stay Informed: The insurance industry is continuously evolving. Subscribe to industry newsletters or follow reputable insurance blogs to stay updated on the latest news and developments.

Engage with Your Insurer: Establish open communication with your insurance provider. Discuss potential discounts, policy updates, and any concerns you might have about your coverage.

Educate Others: Share the knowledge you’ve gained with friends and family who may also benefit from understanding Connecticut car insurance. Your insights could help them save money and avoid potential headaches.

By taking these proactive steps, you ensure not only compliance with state laws but also a comprehensive understanding of the protection available to you. Your car insurance is more than just a legal requirement; it’s a key component of your financial safety net. Remember, the road is unpredictable, but with the right knowledge and preparation, you can navigate it with confidence.

Thank you for joining us on this deep dive into Connecticut Car Insurance. We hope this guide has provided valuable insights to empower your decisions. If you have any questions, comments, or stories to share, please feel free to leave a comment below or reach out to us directly. We love to hear from our readers and are here to help you on your journey.

Until next time, safe travels and happy insuring!

News

News Review

Review Startup

Startup Strategy

Strategy Technology

Technology